- Almost every other Highest-Desire Financing: People mortgage with high interest rate, such as for example pay day loan otherwise store financing, will be a prime candidate having consolidation.

Expertise Family Guarantee for Debt consolidating

Domestic collateral is the difference in their residence’s appraised worthy of and you will the total amount your debt on your home loan. Since you pay down the financial or their home’s well worth grows in the long run, your house security grows, allowing you to control it when needed.

People have access to up to 80% of their residence’s appraised really worth when refinancing. Including, if your house is really worth $five-hundred,000 and you owe $3 hundred,000 on your home loan, you could potentially acquire up to $100,000 to possess debt consolidation. For individuals who borrowed the full $100,000 when you look at the security readily available, you’d be leftover with a mortgage regarding $400,000.

Mortgage refinancing Alternatives for Debt consolidation

With respect to merging loans because of refinancing mortgage, homeowners features a number of different alternatives to take on. These solutions features pros and cons, very finding out how it works will allow you to determine which caters to your specific financial situation.

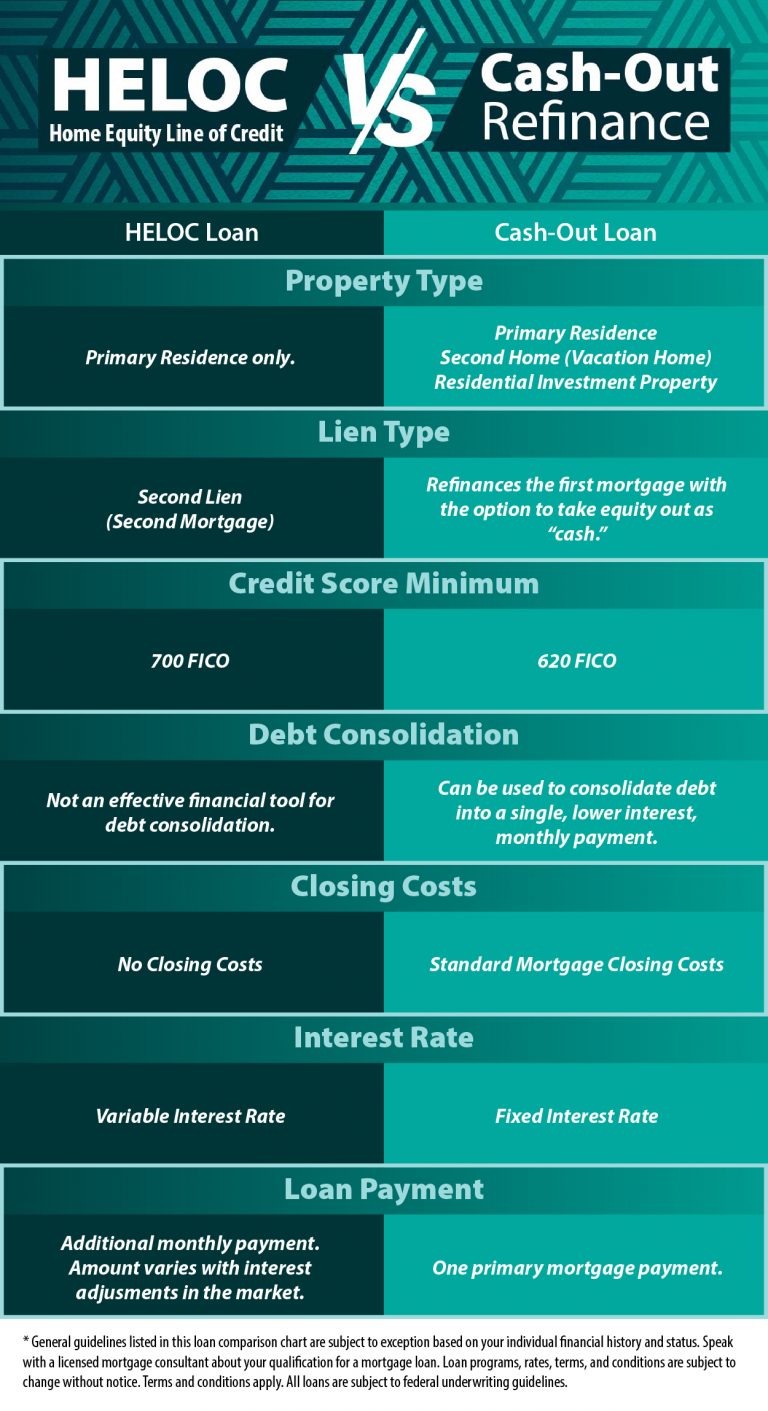

Cash-Aside Refinance

A profit-away re-finance otherwise security takeout (ETO) lets homeowners in order to refinance the home loan for more than they are obligated to pay and you can receive the more amount borrowed into the bucks. You can access up to 80% of house’s appraised worth with no outstanding balance on your newest home loan. The essential difference between your current home https://paydayloansconnecticut.com/cannondale/ loan balance as well as your the fresh new home loan emerges to you personally into the dollars, used to repay your existing debts.

Such as, if the home is worth $eight hundred,000 therefore owe $250,000 on the financial, you can refinance for up to 80% of the property worthy of ($320,000). This allows you to definitely availableness around $70,000 as a consequence of good re-finance. For those who have $fifty,000 in large-appeal debts, you can do a money-aside re-finance to own $300,000 and employ the fresh $50,000 obtain in the dollars to settle those individuals bills.

House Security Credit line (HELOC)

An excellent HELOC are an excellent rotating line of credit covered by your home’s guarantee. Residents can borrow as much as 65% of the appraised value and only pay appeal calculated toward every single day equilibrium. HELOCs try versatile, into the number open to you broadening as you pay down the home loan and certainly will become a great alternative to playing cards.

2nd Financial

A moment home loan enables you to obtain a lump sum facing the house’s guarantee, independent out of your first mortgage. It is recommended otherwise want to split your amazing mortgage contract. An additional mortgage shall be create while the a term loan otherwise a great HELOC.

Rates of interest getting next mortgage loans try high to compensate into most risk on the this financial staying in next status to the first mortgage. Additionally, your own financial must ensure it is a moment home loan trailing its first-mortgage costs.

Refinancing Can cost you Refinancing boasts charges, together with assessment and courtroom. These could make sense and you will negate specific deals from all the way down desire pricing.

A lot more Focus Can cost you If you also continue the newest amortization of your mortgage, you may want to spend even more attention along side longevity of the mortgage, even if your interest and you may monthly obligations try lower.

Likelihood of Losing Your property Combining un-secured debts toward a mortgage places your property on the line if you can’t build payments, as your house is utilized since the collateral.

Actions to help you Combine Personal debt Into the a mortgage Re-finance

- Calculate The House’s Equity Start by deciding your house’s equity. Deduct the quantity you borrowed from on your own home loan from the residence’s appraised otherwise asked valuation.

- Regulate how Far Obligations We wish to Combine Pick hence higher-focus bills we want to become. Determine the total amount to be sure it is in limit accessible using your household guarantee.